The resilience of Iowa residents has been tested this year as the state faced the brunt of major flooding and severe storms leaving a trail of destruction in its wake. Homes, businesses, and entire communities bore the brunt of these natural disasters, highlighting the importance of being prepared as a homeowner in Iowa. Understanding your homeowners insurance policy is the first step in safeguarding your home and family against the unexpected.

The Importance of Understanding Your Homeowners Insurance Policy

Consider your homeowners insurance as a protective shield for your home. It serves as a safety net ready to support you in times of trouble. To fully benefit from its coverage, understanding how it operates is key.

With Iowa’s unpredictable weather, having a clear understanding of what your homeowners insurance policy covers (and what it doesn’t) can make all the difference when navigating through unexpected disasters.

What Does Homeowners Insurance Cover?

Homeowners policies vary based on your individual circumstances and living environment. A standard policy offers comprehensive coverage to protect you from unexpected events, serving as the cornerstone of your financial security. Understanding these policies is crucial in safeguarding your assets and peace of mind.

Dwelling Coverage

This part of your insurance safeguards the structural integrity of your home, including its walls, roof, and foundation. In the unfortunate event of damage or destruction due to a covered incident, your policy would step in to cover the costs of repairs or rebuilding.

Personal Property Coverage

Consider your belongings – furniture, electronics, clothing. Should they suffer damage or theft, rest assured that this aspect of the policy offers protection. This coverage also applies to items stored elsewhere, such as in a storage unit.

Liability Protection

In the unfortunate event that someone sustains an injury on your property, or if you accidentally damage someone else's property and are deemed liable, your homeowners insurance can help cover legal expenses and medical costs.

ALE Coverage

If a storm renders your home uninhabitable, Additional Living Expenses (ALE) coverage steps in to cover the expenses of temporary accommodation. This includes hotel stays, dining out, and any other costs you may need to cover while your residence undergoes repairs.

Types of Homeowners Insurance Policies

When it comes to navigating homeowners insurance, the variety of policies available can be overwhelming. Not all policies are the same, each offering unique coverage tailored to different needs. Let's break it down:

HO-1 Basic Form: This policy is the most basic, covering specific perils such as fire, theft, and windstorms. Due to its limited coverage, it is not commonly used today.

HO-2 Broad Form: A step up from HO-1, this policy includes coverage for additional risks like falling objects and water damage from plumbing issues. While it offers more protection, it still may not cover all potential risks.

HO-3 Special Form: This is the most popular policy, providing broad coverage for your home and other structures on your property. It protects against a wide range of events such as storms, vandalism, fire, and theft, making it a popular choice for many homeowners.

HO-4 Tenant’s Form: Designed for renters, this policy covers personal property and liability, but not the building itself. This is ideal for safeguarding your belongings in a rental property.

HO-5 Comprehensive Form: Offering the most extensive coverage, this policy includes protection against all risks for both the dwelling and personal property, with few exclusions. It typically has higher coverage limits and provides maximum protection.

HO-6 Condo Form: Tailored for condo owners, this policy covers personal property, liability, and improvements to the unit. It addresses the unique needs of condo living, including coverage for the parts of the building you own.

HO-7 Mobile Home Form: Specifically for mobile or manufactured homes, this policy, similar to HO-3, covers the structure and personal property against a variety of perils.

HO-8 Modified Coverage Form: Tailored for older homes, this policy provides coverage for the actual cash value of the property, making it suitable for historic houses with unique construction and higher repair costs.

Selecting the right policy depends on your specific needs and your home. For most homeowners, the HO-3 policy offers a good balance of comprehensive coverage and affordability.

Understanding Policy Limits and Deductibles

Understanding the extent of your coverage and the potential out-of-pocket costs is paramount. This knowledge empowers you to make well-informed decisions regarding your insurance needs for yourself, your loved ones, and your home.

Policy Limits

Policy limits represent the maximum amount your insurance will provide for any covered losses. Ensuring that your policy limits are sufficient to cover the expenses of rebuilding your home and replacing your belongings is crucial.

For instance, if your dwelling coverage limit is $300,000, that is the maximum amount your insurance will allocate for rebuilding your home. Personal property limits typically correlate to a percentage of the dwelling coverage, so it's important to consider this when evaluating your policy limits.

Deductibles

Opting for a higher deductible can lead to lower premiums, but it's essential to choose an amount that you can comfortably handle in case of a loss. For example, if you have a $1,000 deductible and face $10,000 in damages, you'll be responsible for the initial $1,000, while your insurance will cover the remaining costs.

Balancing Premiums and Deductibles

While your deductible represents the initial payment before insurance kicks in, the premium is the cost to maintain your insurance coverage. When deciding on the optimal balance between premiums and deductibles, it's crucial to carefully assess your financial circumstances.

Opting for a higher deductible can result in lower premiums, but it's essential to consider the potential impact of higher out-of-pocket costs in the event of a claim. Take a close look at your budget and emergency savings to determine the highest deductible that you can comfortably manage.

What Isn’t Included in Homeowners Policies?

While homeowners insurance policies typically provide extensive coverage, there are always exclusions to be aware of. Particularly in states like Iowa with unpredictable weather patterns, understanding what is not included in your insurance policy is crucial for financial readiness and considering additional coverage options.

Flood Damage

Unfortunately, flood damage is typically not covered by standard insurance policies. Given Iowa’s history of flooding, it is highly recommended to opt for separate flood insurance. This specialized coverage protects against water damage caused by overflowing rivers, heavy rainfall, or storm surges. In the event of flood damage, there are assistance programs available to aid in recovery for those without comprehensive insurance coverage.

Exploring options such as FEMA assistance (Federal Emergency Management Agency) can provide additional support, although the process may be intricate and often limited to basic needs. Immediate relief for flood damage, including temporary shelter, food, and essential supplies, can also be sought from organizations like the Red Cross. However, it's important to note that these organizations cannot provide long-term financial support.

Mold Damage

Unless mold is specifically caused by a covered event, it is typically not covered by standard homeowners insurance policies. Taking proactive steps such as managing humidity levels and promptly addressing any water leaks is crucial in preventing the growth of mold in your home.

Normal Wear and Tear

A home is meant to be lived in and loved. However, regular upkeep and routine maintenance are not covered in your policy. Homeowners should make sure to budget for these things, as neglect can lead to significant damage that insurance may not address.

Additional Coverage Options

For items not included in your policy, you have the option to explore additional coverages that offer extra protection. Umbrella policies go beyond your standard coverage, providing additional liability protection when you reach your limits, safeguarding you against major claims or legal issues.

Consider securing full coverage for your most prized possessions with riders tailored for high-value items. Whether it's your jewelry, art collection, or unique treasures that exceed standard policy limits, adding riders ensures these valuable items are protected in case of damage, theft, or loss.

This added layer of coverage not only brings peace of mind but also enhances your financial security, especially if you possess substantial assets or valuable belongings.

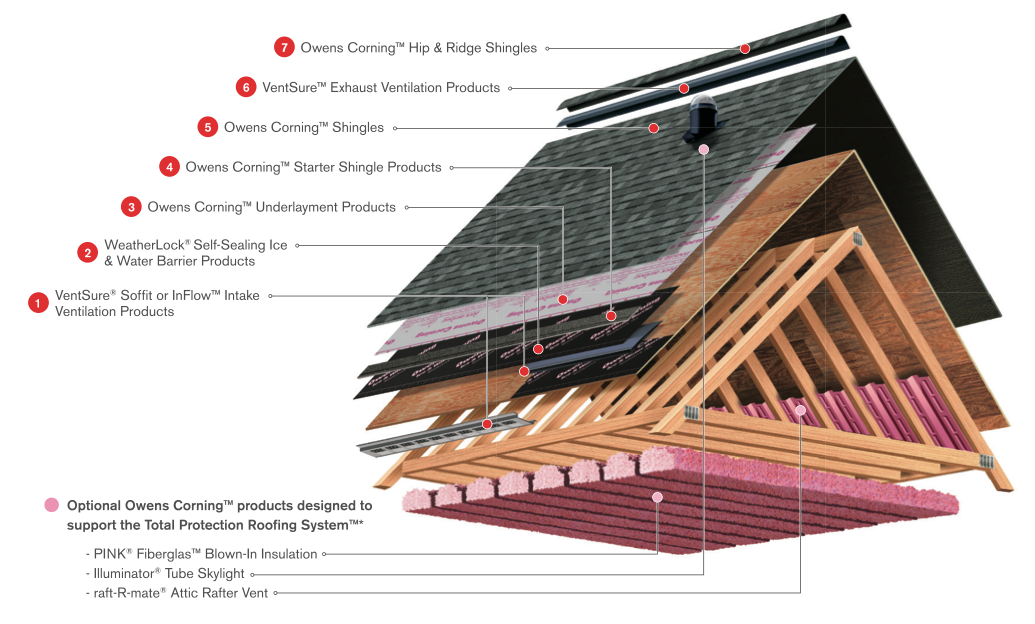

Roof-Specific Coverage

Looking to ensure your roof is adequately protected without any surprises? It all starts with understanding the coverage your roof has.

Standard insurance policies typically cover specific types of roof damage from storms or fire, but the extent of coverage can vary based on factors like the age and condition of your roof. Older roofs may receive less coverage, and some policies might depreciate the value of an older roof, resulting in lower repair payouts.

When it comes to roof coverage, you have a few options to consider. Actual Cash Value (ACV) policies offer coverage based on the depreciated value of your roof, often at a lower cost but with reduced payouts. On the other hand, Replacement Cost Value (RCV) policies cover the full cost of replacing your roof with a new one, providing more comprehensive coverage but at a higher premium.

Filing a Homeowners Insurance Claim

When disaster strikes and your home requires repairs, it's common to rely on your insurance policy as a safety net. However, it's crucial to discern the right moments to file a claim.

Consider filing a claim if the repair expenses surpass your deductible or if the damage is substantial. Yet, steer clear of unnecessary claims to evade potential premium hikes or being labeled as a high-risk client by insurers. Take charge of minor repairs below your deductible threshold. Consistent maintenance plays a pivotal role in preventing claim denials due to neglect or wear and tear. A string of claims within a short span could result in escalated premiums or even policy termination.

Navigating the claims process can be seamless with adequate readiness. Typically, filing a claim involves promptly notifying your insurance provider post-loss. Furnish them with visual evidence like photos and videos depicting the damage, along with any relevant repair receipts you may possess. This meticulous record-keeping not only bolsters your claim but also ensures a fair evaluation. Collaborate with insurance adjusters who will conduct an on-site assessment of the damage, expediting the claims process efficiently.

Maintaining Your Homeowners Insurance Policy

Ensuring your policy remains up-to-date is key to having the right level of protection when it matters most. This involves regularly reviewing your policy, at least once a year, to confirm it aligns with your current needs. Changes in the value of your home or any home improvements you've made might require you to update your coverage from the previous year.

When you embark on significant renovations, such as adding a new room or upgrading your kitchen, it enhances the value of your home. Informing your insurer about these changes could result in additional coverage being added. In some cases, certain improvements might even lead to reduced premiums, like the installation of a new roof or a security system.

Tips for Lowering Your Premiums

Keep in mind, your insurance premium is the price you pay to maintain your policy. Fortunately, there are strategies available to help reduce these expenses while still ensuring you have the necessary protection.

Increase Home Security

Installing alarm systems and enhancing security measures can lead to lower premiums. Deadbolts, alarms, smoke detectors, and other safety features demonstrate to insurance providers that you are actively safeguarding your home.

Bundle Policies

Insurance providers often offer the option to combine policies, such as bundling your home and auto insurance. This can lead to cost savings, as many insurers provide discounts for purchasing multiple policies through them.

Maintain a Good Credit Score

Insurance companies take into account your credit score when calculating your premium, so having a good score can help reduce your rates.

Stay Claim-Free

By staying claim-free over time, you may qualify for discounts on your premiums. While this isn't always within your control, maintaining your home properly can significantly reduce the likelihood of future claims.

Staying Protected

While this article covers a lot, there is always more to learn about insurance. Don't hesitate to reach out to your insurance provider to dive deeper into your coverage and discover ways to keep your home and loved ones secure.

Understanding the nuances of your homeowners insurance policy is vital for maintaining a safe, joyful, and thriving home for years to come. With Iowa's ever-changing weather patterns, being well-versed in your policy details becomes one of the crucial pillars of homeownership. By staying educated and proactive, you can safeguard both your home and your financial stability.

Comments